ENOCH WEALTH Analysis Report 2025: U.S. Economic Landscape and Investment Outlook

- Oct 2, 2025

- 18 min read

By:

George Hsu | Enoch Product Department - Senior Analyst

Erin Lin, CFA, CAIA | Head of Investments

Overview:

The United States of America is the world’s largest economic powerhouse and holds the authority to change the global economic scene in an instant. For investors, many are not certain about the state that America is in, and whether or not it is an opportune moment to invest. Of which, concerns over three key issues: the impact of U.S. tariffs, risks associated with high national debt, and the potential for the dollar to be replaced by other currencies are to be discussed. This report strives to bring analysis based on factual data and ongoing policies to give investors insights into the American market. The report argues that despite current uncertainties, the United States remains a compelling market for investment, offering opportunities in hedging market volatility, capitalizing on policy-supported emerging industries, and leveraging trends in domestic industry reshoring.

Section 1: Macroeconomic Landscape

1.1: Manufacturing

In 2000, the global share of manufacturing output from the United States was at 26.5%, from Japan at 18.1%, from Germany at 7.0%, and from China at 6.9%. In 2024, the four countries still hold around 60% of the world’s manufacturing outputs, with the shares being: China increased to 31.6%, United States down to 15.9%, Japan at 6.5% and Germany at 4.8%.

China's industrial expansion over this period was largely fueled by absorbing shares from the other three industrial powers (U.S., Japan, Germany). Simultaneously, China continuously upgraded its industrial structure and exported labor-intensive, low-to-mid-tier production to other regions (e.g., Southeast Asia).

1.2: Perspectives on the Trade Deficit

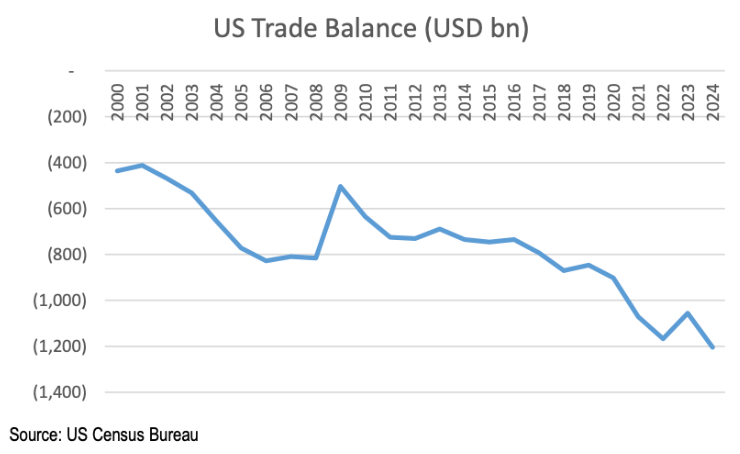

Prior to the 2017 U.S.-China trade war, half of the U.S. trade deficit originated from China. By 2024, China’s share had declined to 25%, meaning that 75% of the shares are distributed by the rest of the world. This is part of the reason why the Trump administration, during the second term, imposed tariffs on every country in the world and not exclusively on China.

The U.S. trade deficit has expanded from approximately $400 billion in 2000 to $1.2 trillion in 2024. There are two perspectives on the trade deficit that the U.S. is enduring. Positively, this deficit corresponds to sustained global demand for dollar-denominated assets like Treasury bonds, granting the U.S. Treasury greater flexibility in debt issuance and the Federal Reserve more room to manage interest rate policy. However, the current high interest rates have sharply increased debt servicing costs, and the potential constraints on Treasury issuance could undermine long-term confidence in the dollar.

1.3: Federal Debt

The U.S. federal debt has escalated dramatically from 30-40% of GDP in the 1980s to 120% ($36 trillion) by June 2025, significantly outpacing the 2024 GDP of $29.2 trillion. Domestically held debt comprises 75% of total Treasury securities, while foreign investors hold 25%, with Japan as the largest foreign holder at just 3.3% of total debt.

The 2024 fiscal deficit reached $1.8 trillion, driven by $6.8 trillion in expenditures that prioritized Social Security ($1.5 trillion), defense ($1.3 trillion), state government affairs ($1.1 trillion) interest payments ($1 trillion), Medicare ($900 billion), health benefit subsidy ($600 billion) and other expenditures ($400 billion). Compared to $4.9 trillion in revenues dominated by income and payroll taxes.

1.4: Share of Global GDP

In 2000, the United States accounted for 30.3% of global GDP, followed by the EU and UK combined at 26.2%, Japan at 14.6%, and China at 3.5%. By 2024, these shares had shifted significantly: the U.S. represented 26.3%, the EU and UK 20.5%, China 16.9%, and Japan 3.8%.

Japan’s nominal GDP reached its closest point to the U.S. in 1995, when it was approximately 73% of the U.S. economy. Similarly, China’s GDP peaked relative to the U.S. in 2021, reaching about 75% of the U.S. size. However, by 2024, China’s nominal GDP relative to the U.S. level had declined to roughly 65%, due to an 11-12% depreciation of the Chinese yuan against the U.S. dollar since 2021.

While the United States wishes to weaken the U.S. dollar to boost export competitiveness, it must avoid excessive depreciation that could undermine the currency’s global utility or severely erode its purchasing power. Moreover, there is a strategic concern that an overly depreciated dollar could accelerate the duration that leads China’s economy to potentially overtake the U.S. on the global stage.

1.5: Money Supply

Since 2000, the U.S. M2 money supply grew approximately fourfold by early 2025, reaching $21.7 trillion. While China’s M2 money supply was 13.6 trillion yuan in 2000 and expanded nearly twentyfold by the end of 2024, reaching 307 trillion yuan (equivalent to roughly 53.5 trillion USD). However, no direct comparison can be made as differences in how M2 is defined in two countries, and in the structure of their financial systems mean these figures are not directly comparable. The U.S. is primarily direct finance-based, meaning a significant portion of assets resides in securities markets rather than bank deposits, thus not fully captured in M2. In contrast, China’s currency is backed by substantial foreign exchange reserves and gold, and its financial system remains bank-dominated and indirect finance-oriented.

1.6: Income Inequality

While the U.S. has experienced overall income growth, the benefits have been disproportionately captured by the wealthiest households. The top 1% of earners now command an average income 139 times greater than that of the bottom 20% population. Since the 1980s, income growth for the top 1% has dramatically outpaced that of the other quantiles.

Section 2: Trump’s Policies and the Line of Logic

Throughout his campaign, Trump consistently reiterated his goals to create high-wage jobs for Americans while reducing the country’s trade deficit and addressing the nation’s high debt burden. Many of Trump’s policies revolve around his plans for economic reform in America.

The line of logic and main goals flows as follows:

Bring industries back to the U.S. for reindustrialization → Creating jobs and reducing the trade deficit → Increasing tax revenue to slash national debt.

Following this underlying logic, many of his actions and headlines revolved around this core theme:

Cracking down illegal immigration could partly result from the goal to reduce labor supply, and thus raise wages for Americans.

Imposing tariffs to force industry reshoring back home

Embracing the traditional energy to stabilize inflation pressure, and choosing the Middle East for his first official visit to ensure international energy prices and U.S. interests.

Linking trade negotiations to domestic investment commitments

Cutting bureaucratic waste and reducing public spending.

The Trump administration recognizes that the global economic system has developed a “path dependency” over the past three decades. By leveraging executive authority, the administration is pursuing a strategy of strategic rule-shifting to implement policies designed to recalibrate global economic architectures in favor of U.S. interests.

This approach mirrors historic moments of the dissolution of the Bretton Woods system in the 1970s, wherein Washington redefined global rules without diminishing the dollar’s centrality, thus ensuring that structural reforms advance national objectives while maintaining international confidence in U.S. leadership.

Section 2.1: Reshaping the External Relations in Trump’s Second Term

The first term of the Trump administration pursued an agenda defined by unilateral policy actions and deregulation, resulting in several significant outcomes. Trump redefined some international relations by signing trade deals and opting out of agreements. As part of the USMCA (or CUSMA which is called in Canada) trade agreement negotiated with Canada and Mexico, the Trump administration secured a key provision requiring that 75% of automotive manufacturing content originate within the U.S. This measure reinforced American leverage in regional trade, with both Canada and Mexico promptly agreeing to the terms.

The Trump administration has pursued an unconventional agenda characterized by rapid execution as seen when the U.S. withdrew from the Trans-Pacific Partnership, the Paris Climate Agreement, and the Iran Nuclear Deal, while pressuring NATO allies to increase defense spending. Most notably, using tariffs as leverage, Trump forced China back to negotiations and secured the Phase One agreement. Overall, American economic and market indicators showed upward momentum during this period in time.

Summary Statistics of Economic Data (2017–2020):

Labor Market:

Unemployment fell from 4.7% in early 2017 to a 50-year low of 3.5% in February 2020.

Approximately 6.7 million nonfarm jobs were added.

Wage growth broke out of long-term stagnation, consistently reaching or exceeding 3% (compared to the previous ~2% trend).

GDP Growth:

Annual GDP growth remained steady: 2.3% (2017), 3.0% (2018), and 2.2% (2019), meeting Trump’s campaign growth targets.

Financial Markets:

The Dow Jones rose from ~20,000 to over 29,000 (pre-pandemic).

The S&P 500 gained nearly 50%, while the Nasdaq surged more than 75%.

This period in time for his first presidential term likely boosted his confidence in swiftly enacting policies in his second term . This is seen when Trump instituted a universal baseline tariff of at least 10% on all imported goods within a week of being in office. On “Liberation Day”, Trump established a reciprocal tariff mechanism that mirrors other nations' import duties or intangible barriers on American products. This approach effectively disregards fundamental disparities in economic scale and development levels, creating an artificially leveled playing field that particularly disadvantages smaller economies despite the United States' dominant position in global production and consumption networks. This policy represents a fundamental reorientation of America's global trade relationships, extending beyond bilateral relations with major partners such as China and Canada to redefine engagement with all trading nations.

These policies collectively represent a strategic departure from multilateral trade principles, particularly through the systematic undermining of the Most-Favored-Nation clause that has underpinned the global trading system since World War II. The administration's approach prioritizes American economic superiority and strategic competition over reciprocal engagement, accelerating the fragmentation of global trade into competing blocs while potentially constraining economic growth in both partner and adversary nations through increased trade barriers and supply chain disruptions.

2.2: Internal Deregulation via The One Big Beautiful Bill Act

The One Big Beautiful Bill Act introduces significant structural changes to the U.S. budget through a combination of spending reductions, targeted investments, and tax reforms. Social programs including Medicaid, food assistance, and state welfare subsidies face substantial cuts and stricter eligibility requirements. These measures are designed to reduce fiscal burdens and improve the domestic tax environment to attract investment. To offset partial costs, new revenue streams are introduced, such as a higher investment tax on private universities and a 1% levy on overseas remittances, alongside expected tariff income.

According to the U.S. Tax Foundation, the plan is projected to stimulate job creation and economic growth, adding nearly 1 million jobs and increasing annual GDP by approximately 0.8% over the next decade. However, the Congressional Budget Office estimates that these measures will also expand the federal deficit by nearly $3 trillion and potentially increase national debt by $3–4 trillion during the same period.

However, it is difficult to truly quantify and estimate the amount of deficit the Big Beautiful Bill Act will incur, since projections rely on statistical and economic models. While logically rigorous, these predictive frameworks operate under the assumption that all other variables remain unchanged, meaning the projections for GDP growth and fiscal deficits hold validity only if the U.S. development trajectory remains consistent. However, this assumption is increasingly untenable under the current administration. The incumbent administration frequently alters policy rules, and information that introduces significant unpredictability, creating substantial margin for error in decade-long forecasts.

2.3: Lower Corporate Tax Rates to Attract Investors

As part of a broader strategy to enhance U.S. economic competitiveness, the current administration has prioritized regulatory reforms, including a significant reduction in the corporate tax rate. The statutory rate currently stands at 21% with President Trump having further indicated support for lowering the rate to 15% for industries and manufacturing operations based within the United States.

The objective of this proposed tax policy is to attract and retain business investment, strengthen domestic supply chains, and position the United States as one of the most attractive jurisdictions for corporate operations globally. This initiative reflects the administration’s commitment to using fiscal policy as a tool for industrial reactivation and long-term economic realignment, even as debates continue concerning the trade-offs between tax incentives, federal revenue, and fiscal sustainability.

2.4: Federal Workforce Reduction

As part of its broader deregulatory agenda, the administration has reduced the federal workforce by approximately 300,000 employees across multiple agencies. This streamlining effort is strategically aligned with policies aimed at reducing regulatory barriers to stimulate investment in the United States. The reduction in personnel has been coupled with the restructuring or elimination of specific regulatory bodies, resulting in:

Deregulation in financial sectors such as hedge funds and private equity, and a likely permission for retirement accounts to invest in alternative assets.

Streamlined approval processes for AI infrastructure projects and loosened restrictions on AI development and deployment.

A more favorable market environment for cryptocurrencies.

Relaxed policies for traditional energy production and eased environmental regulations.

Simplified export rules for military equipment.

2.5: The Federal Debt Problem

The Trump administration's economic strategy leverages a combination of tariff policies, regulatory reforms, and tax restructuring to address federal debt sustainability. A key component of this strategy involves revising tax policies to lower overall tax rates while broadening the tax base. By increasing the number of taxpayers rather than raising individual tax burdens, the administration aims to generate additional government revenue to decrease the overall federal debt.

Historically, U.S. federal debt has been treated as a zero-risk investment, under the assumption that the United States will not default. The issuance of this debt traditionally exhibited an inverse relationship with the federal funds rate: borrowing expanded during low-rate periods to lock in affordable financing and contracted during high-rate periods to avoid excessive costs. The current environment, however, marks a sharp departure from this pattern. Despite the federal funds rate remaining elevated near 4%, debt issuance continues to accelerate rapidly, driven by persistent structural deficits.

2.6: When is the Federal Debt a Problem?

The sustainability of U.S. federal debt is evaluated through three aspects: domestically held debt, debt burden relative to economic capacity, and interest rates. Domestically held debt, approximately 75% of total U.S. Treasuries, reduces external vulnerability and reinforces stability through aligned domestic incentives. The debt-to-GDP ratio, standing at approximately 100-110% when excluding Federal Reserve holdings, remains within manageable bounds compared to critical thresholds (160-200%) identified by institutions such as the IMF and Penn Wharton Budget Model. Lastly, the monetary policy environment, particularly the level of interest rates, directly impacts debt servicing costs and refinancing risks. Current elevated rates present fiscal challenges, though the Federal Reserve’s capacity to lower rates remains key in preserving medium-term debt sustainability.

Driven by emerging economic risks, the Trump administration has intensified its calls for the Federal Reserve to cut interest rates. This push is grounded in several key factors: interest payments on the national debt now consume 14% of the federal budget, exceeding the defense spending of 13%. Inflation has significantly cooled to 2.7% in July 2025 from its 9.1% peak three years earlier, at the same time, the unemployment rate has begun trending upward, reaching 4.2% in July.

Despite the recent fear of the federal debt, U.S. Treasury securities continue to be perceived as low-risk assets by global investors, at least for the time being. The U.S. dollar's role as the world's dominant reserve currency, facilitating over 80% of foreign exchange transactions, nearly half of global trade settlements, and comprising approximately 60% of central bank reserves. This creates inherent demand for dollar-denominated assets. This is further reinforced by the liquidity of the Treasury market, where daily trading volumes exceed $1 trillion, providing investors with unmatched flexibility. The transparent and independent legal regime also fortifies investors’ confidence.

Section 3: Cryptocurrencies Introduction

The cryptocurrency market has matured over the last ten years, establishing itself as a legitimate asset class for global investors. Bolstered by supportive regulatory policies, particularly in the United States, and its expanding adoption, market confidence in digital assets has reached unprecedented levels. This raises concerns on whether the U.S. Dollar would be replaced, as cryptocurrencies largely flow unregulated throughout the globe.

3.1: Government Policies to Assist the Position of the U.S. Dollar

Signed on the 18th of July, 2025, The GENIUS Act, or the Guiding and Establishing National Innovation for U.S. Stablecoins Act, mandates that stablecoins must hold 100% liquid reserves and publicly disclose the composition of these reserves monthly. These reserves cannot be pledged or rehypothecated. Additionally, the Act defines the stablecoins as digital assets, rather than digital currency nor fiat money, and prohibits these digital assets to perform any types of investment or financing functions. Thereby, forcing stablecoins to be tethered by the U.S. Dollar and not as a replacement.

Moreover, The Digital Asset Market Clarity Act was signed to categorize digital assets into digital commodities (highly decentralized, deriving value from blockchain systems with minimal reliance on issuers) and digital securities (representing ownership bonds or investment contracts meeting specific criteria). The distinction clarifies the regulatory jurisdiction between the Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC). In addition, the Anti-CBDC Surveillance State Act was signed to prevent the Federal Reserve from issuing a central bank digital currency (CBDC). These policies are in support of the innovation of digital assets, and the adoption of the dollar-backed stablecoins to modernize payments and allow for the U.S. Dollar to be widespread in the digital market.

3.2: The Example of the HKD

In Hong Kong, banks must hold a 1:1 USD reserve at a fixed exchange rate of 7.8 HKD to 1 USD when issuing HKD. This ensures that the HKD has long term stability, but it relinquishes monetary autonomy. This is similar to how the U.S. is attempting to back its stablecoins with the dollar, effectively extending the influence of U.S. monetary policy to digital currency and asset markets. By leveraging its regulatory power to solidify the dollar’s role in the digital age, it allows the USD to mirror the structural dominance of the Hong Kong USD peg. This also allows for the U.S. monetary policies to indirectly penetrate the global digital market.

In countries facing hyperinflation crises (e.g., Venezuela, Nigeria), individuals or businesses may become more inclined to adopt the dollar-backed stablecoins for transactions instead of the currency supplied from their central bank. In taking advantage of the weakening monetary values of developing countries, the United States will attempt to control and strengthen demand for the U.S. dollar. Stablecoins issued by other countries may struggle to compete with USD-backed stablecoins due to limited types of eligible reserve assets and less robust regulatory frameworks.

3.3: Historical Examples of Attempts to Back Other Commodities with the Dollar

The United States is known to be a trailblazer in the global economy. After the U.S. dollar abandoned the gold standard in 1971 under President Nixon, many were skeptical of the U.S. dollar and its power within the global economy. However, the U.S. then regained the demand for the dollar by reaching an agreement with Saudi Arabia during this period to designate the U.S. dollar as the pricing currency for oil (Petrodollar). By anchoring the dollar to crude oil, the system ensured that all oil-importing countries needed to hold dollars as foreign exchange reserves to facilitate transactions.

3.4: Solidifying the Dominance of the U.S. Dollar

The three major U.S. digital asset bills will facilitate the development of stablecoins and tokenization, while the underlying tokenized assets will be backed by real-world collateral. Supported by the new policies, a piece of real estate, a part of an office building, stocks, bonds, the USD-pegged digital tokens can be tokenized as real-world assets (RWA). This expands the range of tradable digital assets anchored to the USD, enhancing its utility in decentralized finance markets. The U.S. is attempting to tie most of tangible assets to the dollar as its end goal. Although multiple blockchain platforms are competing in the tokenization market, over 99% of the global stablecoin supply (approximately $250 billion) is USD-backed, and thus competing attempts would be inconsequential.

3.5: The Logic of Total Dominance

Current U.S. policy reflects a strategic pivot to reinforce the U.S. dollar hegemony through both traditional economic levers and digital innovation. Imposing tariffs and enacting tax cuts are steps to attract corporate investments. However, recognizing that a narrower trade deficit could constrain traditional avenues for foreign entities to reinvest back into U.S. markets. Therefore, the U.S. is taking steps in tokenizing their assets, as it can now attract capital from the global crypto economy by offering tokenized pieces of American property and infrastructure, ensuring a steady flow of capital and reinforcing the dollar's strength. By offering fractional ownership of American assets through blockchain technology, the U.S. ensures a continued inflow of foreign capital, thereby supporting the dollar’s strength as well as the value of American assets.

3.6: Concerns for Investing in the United States

This report highlights three primary concerns: tariffs, the national debt, and the potential replacement of the U.S. dollar. Tariffs present a strategic tool; while globally disruptive in the short term, they could be leveraged by the U.S. to attract investment and reduce national debt. If the investment strategy outlined in the previous section is successfully realized, tariffs could serve as an effective tool for reducing the national debt. Concerning the national debt, current risk remains low due to sustained international demand for U.S. assets. Its long-term stability, however, is contingent upon federal budgetary reforms and the revenue-generating efficacy of newly enacted legislation, such as the strategies discussed in Section 1.5. The U.S. Dollar's position remains secure for the coming decades. Its resilience, innovation in digital currency, and unparalleled international demand create exceptionally high barriers for any potential competitor.

Section 4: The American Investment Landscape

Since the Trump administration took office, the global economic landscape has been marked by heightened uncertainty, market volatility, and increased political influence over economic affairs. This environment has led many investors to reconsider investment activities in the United States. The following analysis delves deeper into the implications of these developments for the U.S. market and identifies the core ideas of the current policies.

4.1: Redefining the Rules for the 401(k)

The Trump administration on August 7th, 2025, announced to democratize access to alternative assets for all 401(k) investors. The policy change would likely allow Americans more diversified investment options and attain stronger and more financially secure retirement outcomes through options such as real estate, cryptocurrencies, and private equity. Details for the plan are available starting early 2026. From the directions of these policies, we believe that the market's new capital flowing into alternative assets, on a relatively conservative estimate, could range from $600 billion to $1.2 trillion.

4.2: Hedge Funds in Relations of Downside Risk

Hedge Funds Targeting Absolute Returns (α): Unlike mutual funds, which primarily seek relative returns (β) (aiming to outperform the market in bull conditions and minimize losses during bear markets), hedge funds employ α-driven strategies designed to generate positive returns regardless of market conditions. This approach is particularly effective in environments heightened uncertainty and elevated correction risks, enabling them to deliver excess returns. This approach also allows the volatility to be lower when compared to traditional stocks and bonds.

An analysis of the worst 10 months for equities and bonds over the 10-year period ending December 2024 reveals the HF Composite's role as an effective diversifier and risk mitigator. Hedge funds generate alpha even during periods of bond market stress. The most pronounced example occurred in the year of 2022, where the HF Composite's drawdown was limited to -2.4%, significantly cushioning portfolios against the equity market's -20% decline.

SUMMARY: Finding Certainty in the World of Uncertainty

In a world of uncertainty, we identify the following core certainties shaping the U.S. economic landscape:

Policy uncertainty under the Trump administration will continue to drive market volatility. In addition, the U.S. stock market has repeatedly hit new highs since June-August, leading investors to grow increasingly cautious about mounting correction risks.

U.S. policies will continue to support AI and cryptocurrencies to focus on maintaining the U.S. dollar hegemony. Recent domestic regulatory relaxation continues to solidify American leadership in emerging technologies and assets. Creating a more favorable environment for AI infrastructure investments, cryptocurrency issuers, and trading platforms.

Industrial reshoring and rising domestic investment. U.S. tariffs are explicitly tied to commitments for domestic investment, making it clear that corporate reshoring will drive new demand for residential and industrial real estate.

RISK DISCLOSURE

Investing in securities and other financial products involves a variety of risks that may result in partial or total loss of principal. The strategies and market insights discussed herein are subject to, among others, the following risks:

Market Risk: The value of securities can fluctuate daily due to economic, political, and market-specific factors. There is no assurance that any investment strategy will achieve its stated objectives.

Liquidity Risk: Some investments may be less liquid than others or illiquid, meaning they might be difficult to sell within a reasonable timeframe, or without significantly impacting their price, potentially preventing a sale at or near their stated value.

Capital at Risk: Some investments may include a high degree of risk, including the possibility of total capital loss. Investors may not recover the initial amount invested, and past performance is not indicative for future returns, as actual outcomes may differ materially from historical results.

Credit and Counterparty Risk: The possibility exists that issuers or counterparties may fail to meet their financial obligations.

Currency and Political Risk: Investments in foreign markets may be adversely affected by fluctuations in currency exchange rates, changes in governmental policies, or political instability.

Concentration Risk: Non-diversified portfolios, or those concentrated in a specific sector or asset class, may experience higher volatility if conditions affecting that area deteriorate.

Derivatives and Leverage: The use of derivative instruments or leverage can amplify both gains and losses, and may introduce additional risks including valuation, correlation, and counterparty risks.

ESG and Impact Investing Considerations: Strategies that incorporate Environmental, Social, and Governance (ESG) or impact investing factors may underperform relative to broader market benchmarks if market sentiment shifts against the favored sectors or themes.

Lack of Information or Operating History: Investments in exempt securities with limited operating histories or information may carry additional risk, as there may be insufficient data to assess the stability, performance, or management track record. The absence of a proven history increases the uncertainty and potential for unforeseen challenges.

Investors should be aware that these and other risks can cause investment results to vary significantly from the objectives set forth in this publication. No assurance is given that any investment strategy or market insight will be successful, and all investments carry inherent risks, including the potential loss of principal.

IMPORTANT NOTICE

The views and opinions expressed herein are solely those of the author(s) as of the publication date and do not necessarily reflect the views of Enoch Wealth Inc. or its affiliates. This material is not intended for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to applicable laws or regulations. Recipients of this material should ensure that they comply with all relevant local legal and regulatory requirements.

Before acting on any information contained in this publication, readers should consider their own financial situation and risk tolerance and seek independent professional advice as necessary.

DISCLAIMER

The information contained herein is for general informational and educational purposes only and does not constitute an offer, solicitation, or recommendation to buy or sell any securities or financial products. The market insights, opinions, and analyses expressed in this publication are those of the author(s) as of the date of publication and are subject to change without notice. They are not intended to be, and should not be construed as, personalized investment advice or a substitute for professional advice tailored to your specific financial circumstances. Neither Enoch Wealth Inc. nor its affiliates shall have any liability or obligation to any party for any loss or damage arising directly or indirectly from the use of, or reliance on, the information provided herein.

Investors are advised to perform their own due diligence and consult with an independent financial advisor, accountant, or attorney before making any investment decisions. Past performance is not indicative of future results, and no representation is being made that any account will or is likely to achieve profits or losses similar to those reported.